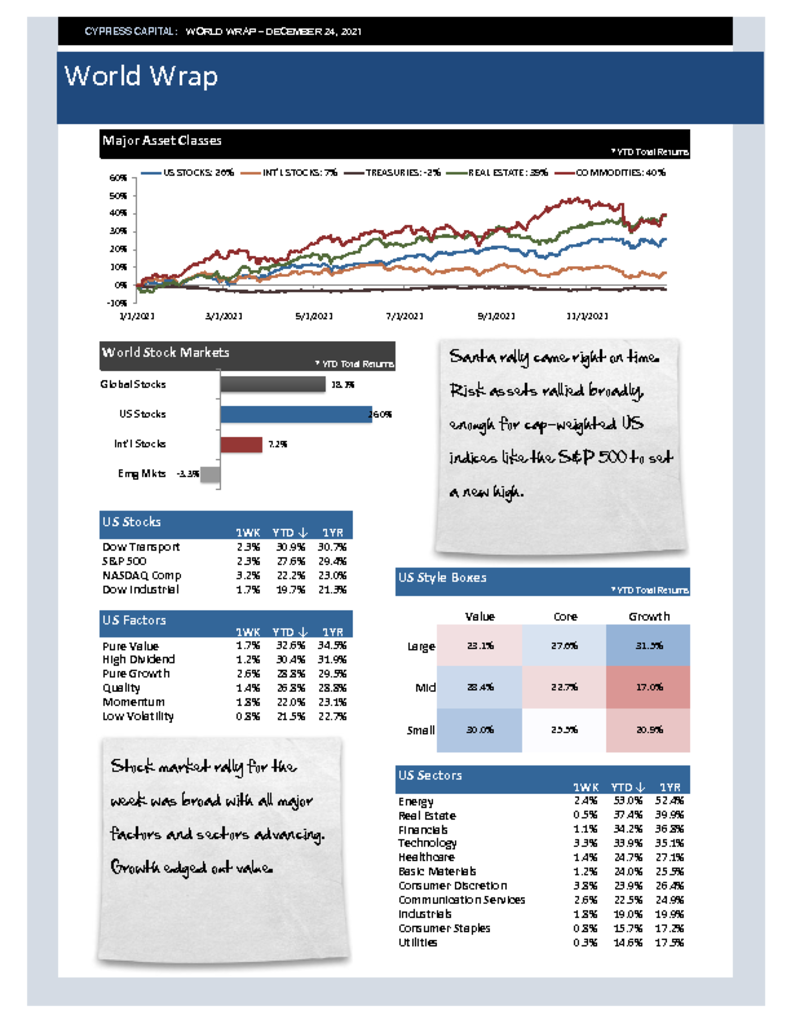

– Santa rally came right on time. Risk assets rallied broadly, enough for cap-weighted US indices like the S&P 500 to set a new high.

– Stock market rally for the week was broad with all major factors and sectors advancing. Growth edged out value.

– Emerging markets moved higher but not impressively. China was flat and down more than 22% in 2021.

– Commodities bounced back as did Bitcoin, while Treasuries gave up recent gains.